Inside x402: Mapping the First Wave of Agent Payments

Introduction

This report positions x402 as an emerging agent-native payment rail where card-like UX meets on-chain settlement.

In practice, the space is still so early that the current model effectively mirrors USDC on Base, with only a few intermediaries, like Coinbase CDP and Questflow, bridging activity. Here, economic actors include humans, AI agents, and on-chain liquidity working together.

We focus on what is actually happening on-chain today, using Base as the primary hub for x402 transactions and grouping wallets into “agent-like” vs “human-like” clusters based on their behaviour.

Report Key Takeaways & TLDR:

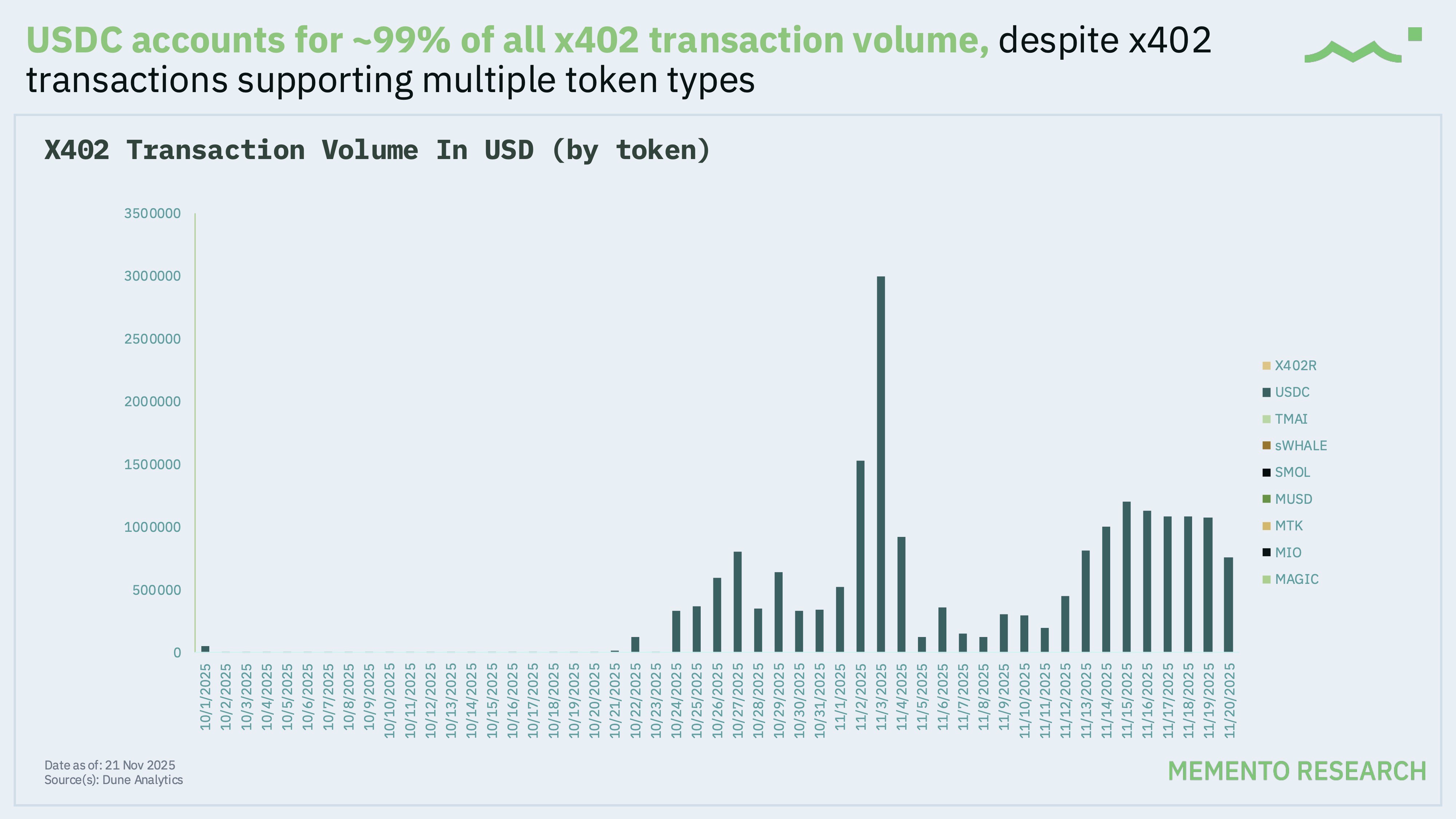

USDC dominates x402: although x402 supports multiple tokens, about ~99% of recorded volume settles in USDC today

Base as the main chain: Base accounts for ~89% of x402 transaction share, making it the de-facto execution environment for the standard so far

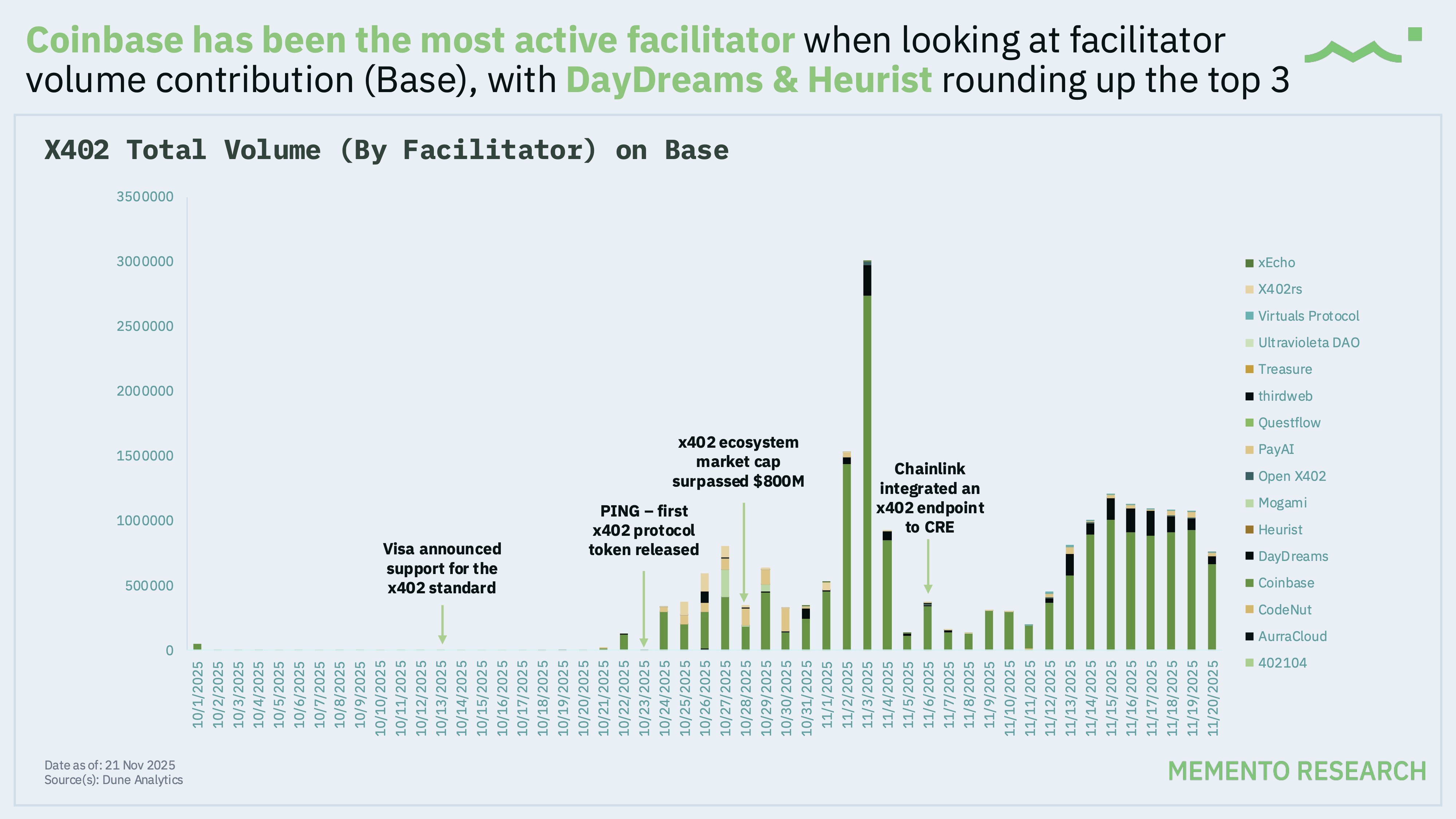

Facilitator hierarchy: Coinbase remains the most active facilitator by transaction count, while Questflow consistently routes payments to the widest set of service providers

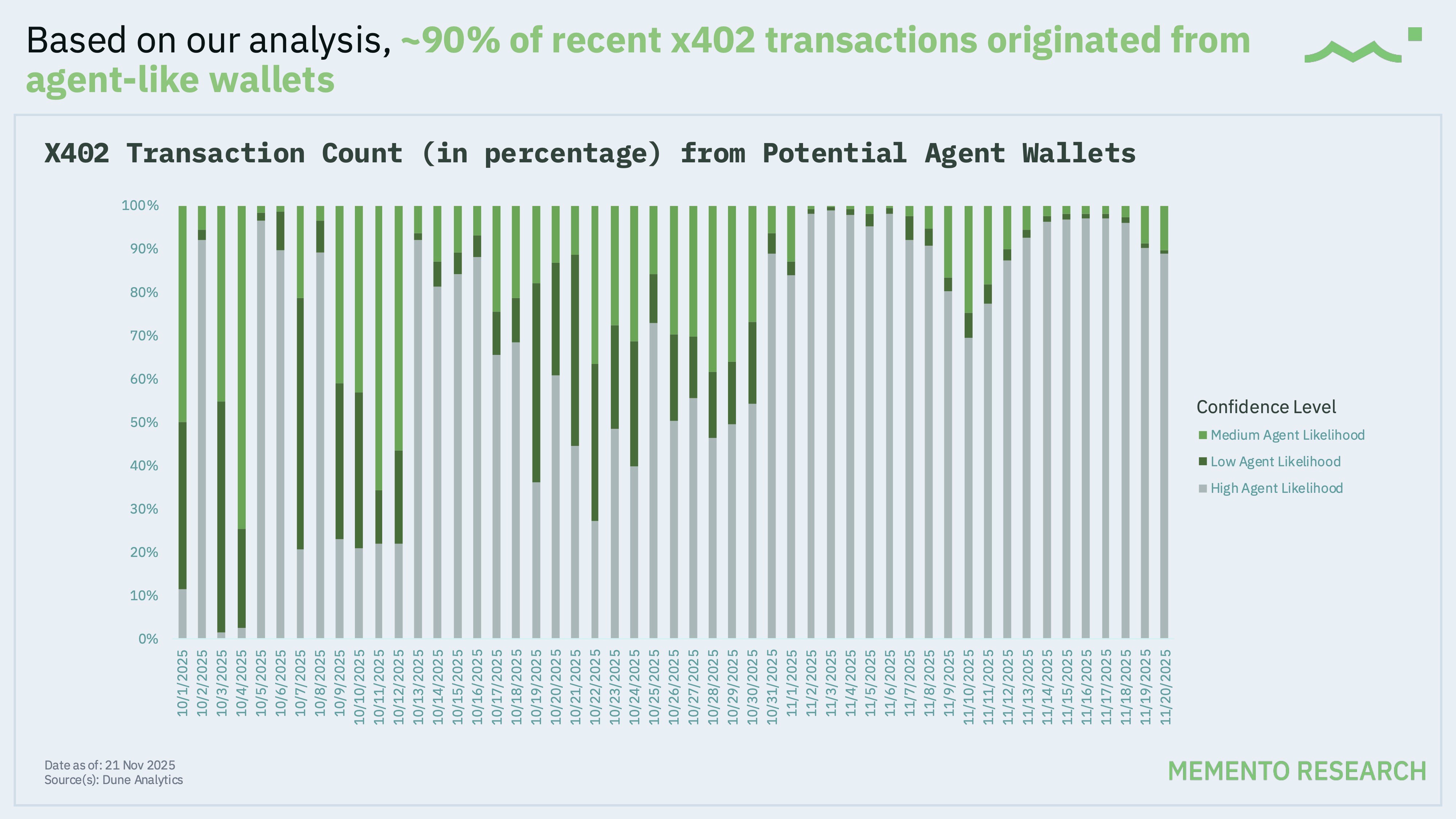

Activity heavily facilitated by AI Agents: ~90% of recent x402 transactions come from wallets that look and behave like automated AI agents, not humans (data based on transaction frequency, size and history)

Methodology on How We Infer “Agent-like” Wallets

To understand who is actually using x402, we cluster wallets by their on-chain behaviour and label them as “agent-like” vs “human-like” using a simple scoring system. For every original sender address, we assign up to 3 points based on:

High activity: Wallet has >500 total transactions → +1 point

Small ticket sizes: Average USDC per transaction < 2.5 USDC → +1 point

High frequency: Average time between transactions < 1.5 minutes → +1 point

Addresses with higher scores are treated as more likely to be agents or heavily automated flows, while low-score addresses are more likely to be humans or low-frequency app wallets. We then analyse volume and transaction counts across these confidence bands (Humans dominated, Mixed pattern, Agents dominated).

This is intentionally conservative: the goal is not perfect classification, but a directional picture of how much of x402 usage is already machine/AI-driven.

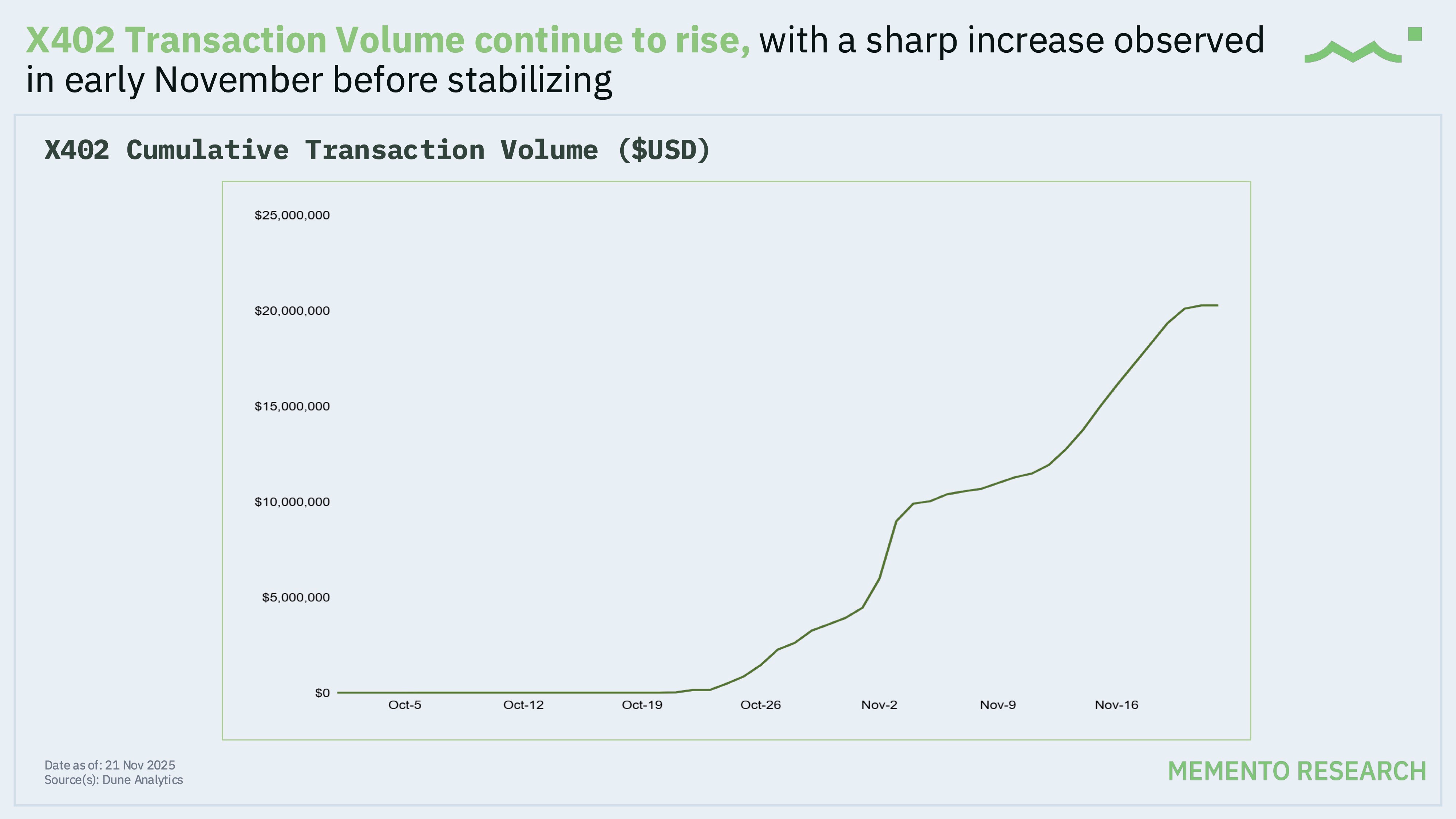

Market Overview and Recent Milestones

x402 has moved from a theoretical concept to actual payments on-chain quite quickly. In the last year, several events have pushed it from niche “agent payments” concept into a small but real ecosystem:

Visa announced support for the x402 standard, signalling that TradFi payment networks are willing to experiment with agent-to-agent commerce

Google also announced their Agent Payments Protocol (AP2) → an open, shared protocol that provides a common language for secure, compliant transactions between agents and merchants

PING launched as the first dedicated x402 protocol token, giving the ecosystem a native asset for incentives and governance

Chainlink integrated an x402 endpoint into its Chainlink Realtime Engine (CRE), fitting x402 into their existing infra that is used already by many dApps

In the era of modern blockchain infra and tooling, the role that agent to agent payment plays is multi-fold:

Programmable Accounts/Smart Contracts: Agents are usually represented by contract accounts that can sign or authorize transfers

Gas Sponsorship/Paymaster Models: One agent can cover transaction fees for another, essential for seamless automation (helpful for onboarding new users onto the blockchain)

Cross-Chain Messaging - Protocols like IBC, XCM, or Wormhole let agents on different chains pay each other without manual bridges

How an x402 Payment Works

Before diving into the data, we need to set the context. Every x402 transaction interfaces with four economic actors:

Client/Buyer (Sender): a human, AI agent, or application that wants access to some paid resource (API call, model output, content, service)

Server/Seller (Recipient): the API provider, content creator, or service

Facilitator: a third-party infra provider like Coinbase that verifies the HTTP 402 “payment required” intent, handles off-chain auth, and pushes the actual settlement transaction on-chain.

Blockchain network: the settlement layer where the transaction takes place on

TLDR: Think of facilitators as mini card networks for agents: they abstract signing, key management, and fee logic away from both client and server while still settling in public stablecoins.

The reason the live data shows near-total reliance on USDC (~99% of x402 transaction volume) is because of:

ERC-3009/transferWithAuthorization: USDC implements this pattern, which aligns neatly with x402’s “authorization then settle” flow

Native support in Coinbase CDP and Base: Coinbase’s own facilitator stack and Base as an L2 are optimised for USDC, so tooling, risk checks, and liquidity all skew in its favour

Price stability & compliance: for agents and enterprises, volatile assets add more operational complexity; stablecoins with clear regulations minimise it

Facilitators

On Base, Coinbase remains the most active facilitator by raw transaction count, underlining its role as the main infra layer for early x402 adoption.

However, when you slice by active senders per facilitator, the landscape is more competitive:

Coinbase now shares user dominance with PayAI and DayDreams, indicating that some specialised facilitators have managed to build meaningful client bases and partnerships of their own

Heurist appears as a new challenger, suggesting that the facilitator layer is still in a discovery phase where new entrants can win niches or by offering competitive rates

A separate view of transaction volume by facilitator shows Coinbase still controlling a large share of dollar-flow, but with noticeable contribution from DayDreams and others.

Takeaway: Agents and apps are not locked into a single facilitator; they route through whoever offers the right blend of UX, limits, and integration surface.

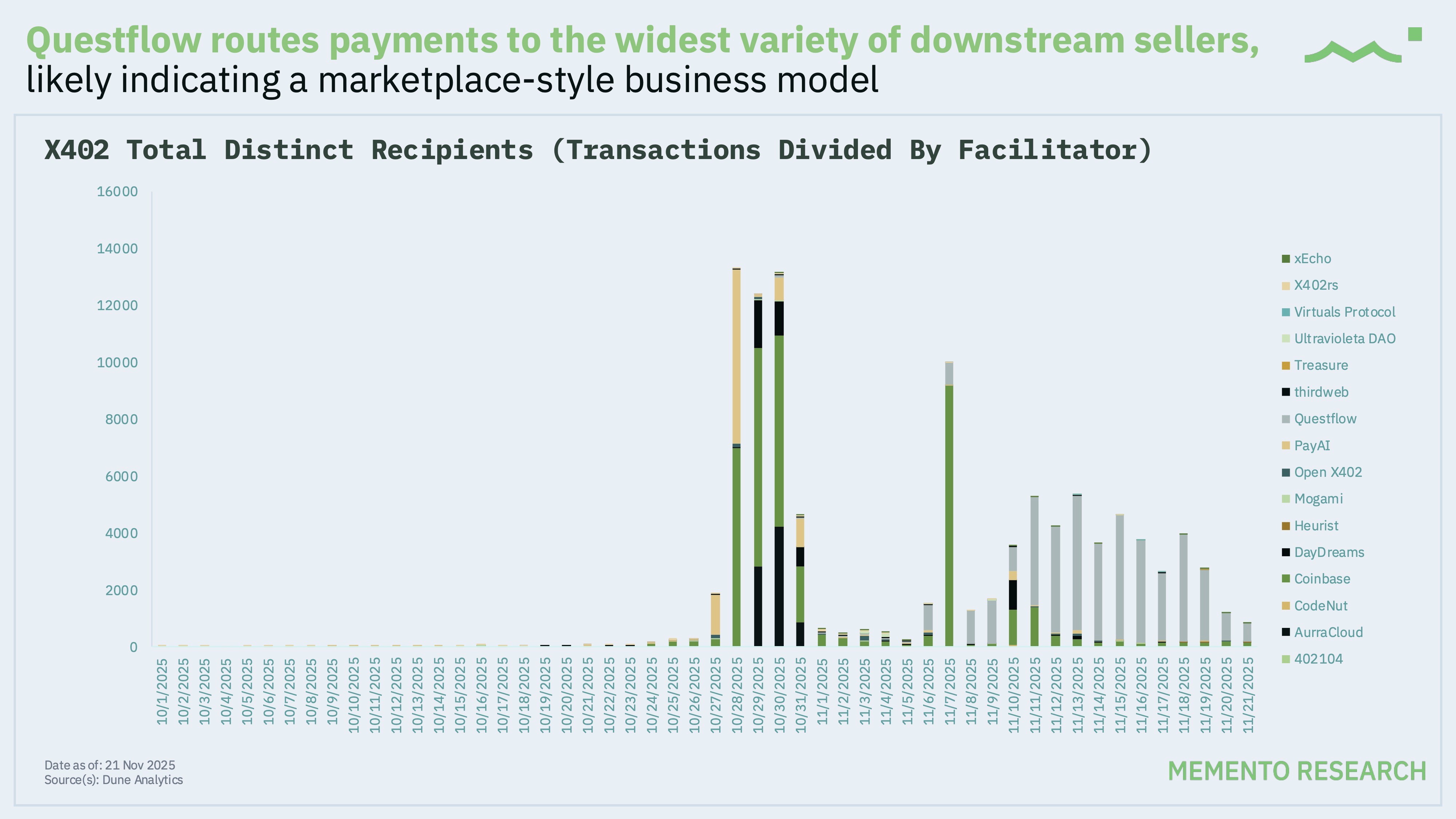

Recipients: Where Does the Money Actually Go?

While Coinbase dominates as a facilitator, Questflow stands out on the recipient side where it consistently demonstrates the most decentralisation in payment receivers (service providers).

The data shows that:

Questflow routes payments to the widest variety of downstream sellers, indicating a marketplace-style model where many independent providers plug in

Other facilitators tend to have more concentrated recipient sets

From an ecosystem health perspective, Questflow looks like the “long tail” aggregator for x402, while other facilitators function more like vertical SaaS rails with a smaller supplier set

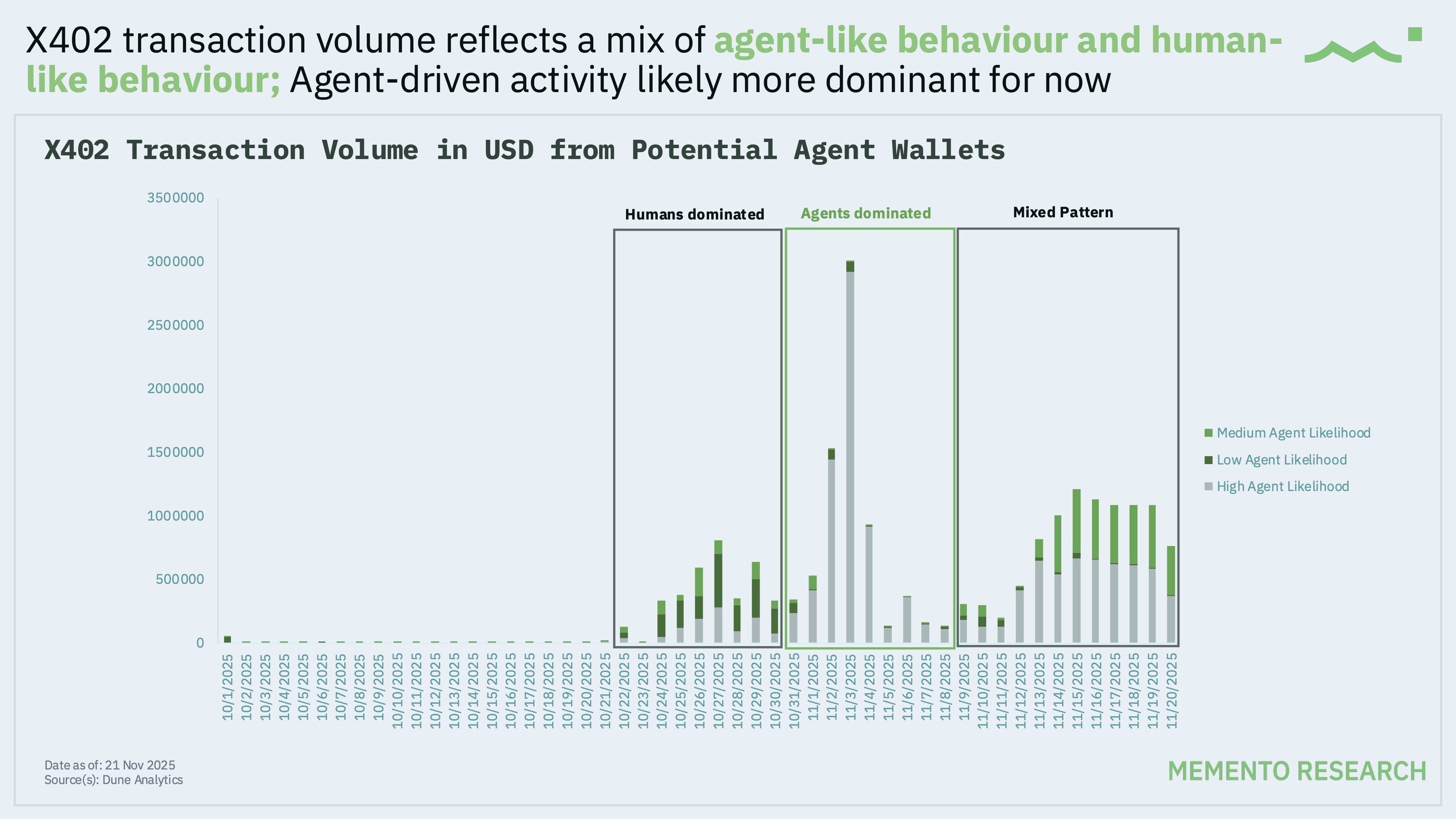

Who’s Paying: Agents vs Humans

x402 transaction volume is already a mix of agent-like and human-like wallets, but skewed towards the former.

Volume split → the “Transaction Volume from Potential Agent Wallets” chart shows 3 patterns across facilitators and time windows:

Zones where humans dominate: usually lower frequency, larger-ticket transaction

Mixed zones: hybrid flows where human-initiated sessions trigger a burst of automated calls.

Segments where agents clearly dominate, with dense streams of small USDC payments → agents are meaningful contributors to dollar volume

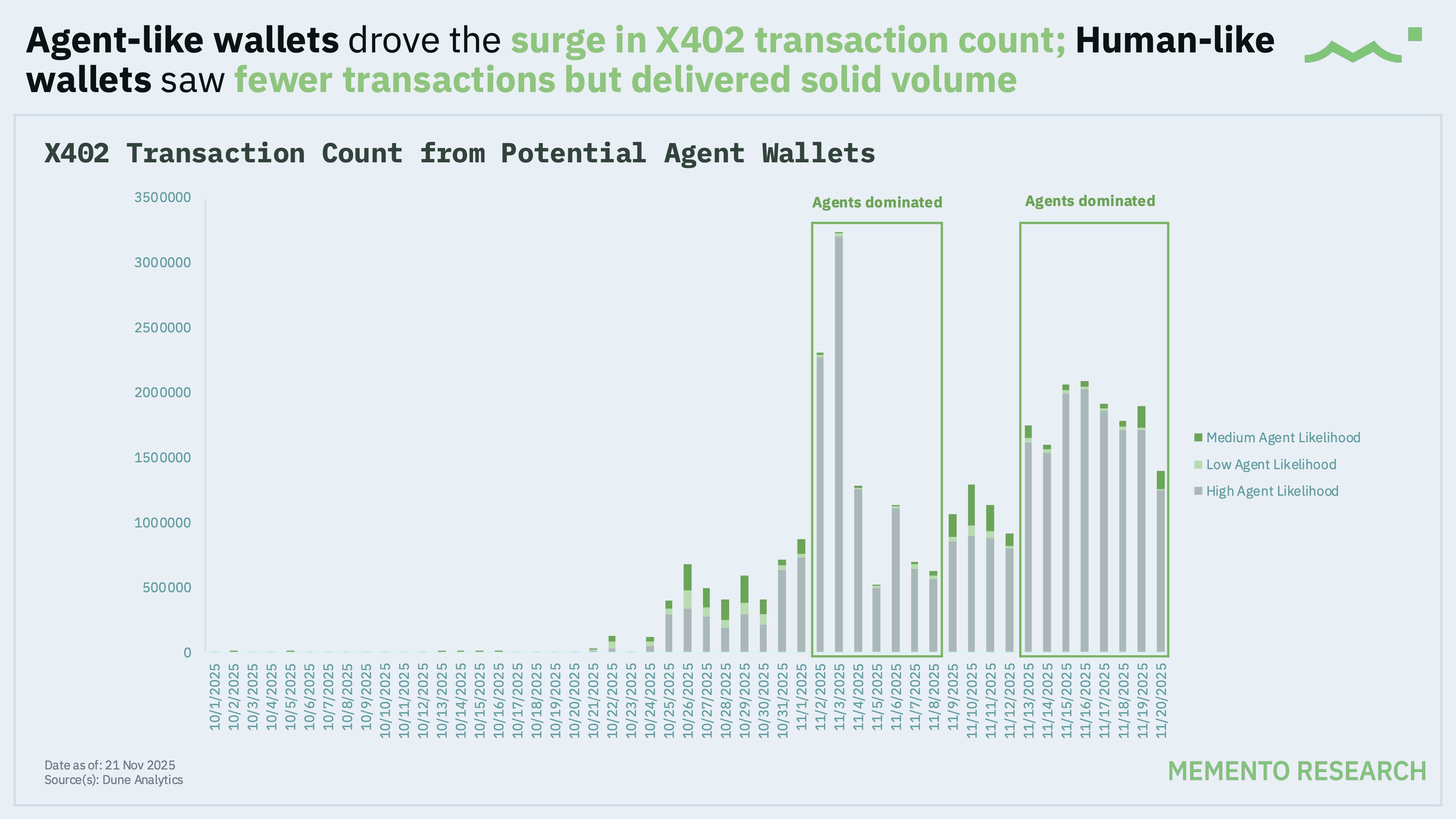

Transaction counts → Where agents really take over is transaction count. The data shows:

The surge in x402 transaction count is driven primarily by agent-like wallets

Human-like wallets have a much smaller share of total transactions, but when they do transact, the average ticket size is larger, so they still contribute a non-trivial share of volume

In recent windows, agent-like wallets account for ~90% of all x402 transactions by count

Takeaway: Agents generate thousands of tiny micro-payments, while humans show up for less frequent, higher-value actions (subscription-style, enterprise usage, or developer testing)

Data & Confidence Bands

We further break volume down by confidence level to show how many of the behavioural criteria each wallet satisfied to see how robustly “agentic” the flow is.

Simply put, even under strict assumptions, a lot of x402 looks like machines paying machines.

Base Concentration & Ecosystem risk

All of the x402 activity thus far is heavily concentrated on Base, which handles roughly 89% of x402 transactions. This has two immediate implications:

Good for UX today: one canonical chain means less fragmentation for infra teams, indexers, and explorers. Liquidity and tooling compound faster

Risk of over-reliance: if agent commerce meaningfully scales, over-reliance on a single L2 + a single stablecoin (USDC) introduces platform and chain risk. Any disruption in Base or USDC directly impacts the ability of agents to pay and get paid.

As x402 matures, watching expansion beyond Base / USDC will be as important as tracking volume growth itself.

Conclusion

x402 tech is already live, yet remain overwhelmingly USDC on Base. USDC accounts for ~99% of x402 volume, with Base as the main settlement corridor thanks to ERC-3009 support and deep Coinbase integration

Facilitators are the new “mini networks”. Coinbase leads by transaction count, but sender activity is also shared with other competitors, suggesting space for differentiated rails rather than a single winner

Questflow is looking most likely to be the marketplace bet. It consistently routes payments to the broadest set of recipients, positioning itself as the long-tail service layer for x402 while others prioritise depth with fewer partners

Agents already dominate transaction flow, generating ~90% of x402 transactions, while humans handle fewer, larger-ticket payments

Concentration is both a feature and a bug. The same design choices that make x402 smooth today (USDC, Base, Coinbase CDP) create future dependencies. The next phase of this narrative is whether volume spreads across chains, stablecoins, and facilitators

Today, x402 looks simple on the surface → since almost everything is USDC on Base, routed through a small set of facilitators.

Our data findings show that this already resembles an early machine-to-machine payment rail where agents generate most of the transactions. Questflow is aggregating a long tail of providers, and new facilitators are quietly chipping at Coinbase’s lead.

What remains to be seen is whether x402 can broaden beyond USDC + Base and make it the default way software pays for software.